Earnings Season Is Time To Park Cash in ETFs' Puts & Covered Calls

Earnings surprises can stick traders with big losses on cash secured puts and covered calls. ETFs will be less risky than a lot of volatile stocks during July.

By Donald E. L. Johnson

Cautious Speculator

Key points:

Many risk averse investors do not have open puts or calls trades positions when companies publish their quarterly financial reports and update their guidance.

During earnings season an ETF’s price is not moved much when one or more of the companies in its portfolios surprises them with better than expected or disappointing financial reports and guidance.

That is why it often pays to put part of a portfolio in ETFs during earnings season. Major surprises and a series of surprises and other news can move markets and ETFs, but they don’t move as much as individual stocks often do.

Active traders of covered calls stock and ETF options can diversify their earnings season risks by going to cash, money markets or selling covered calls and cash secured puts on underling exchange traded funds.

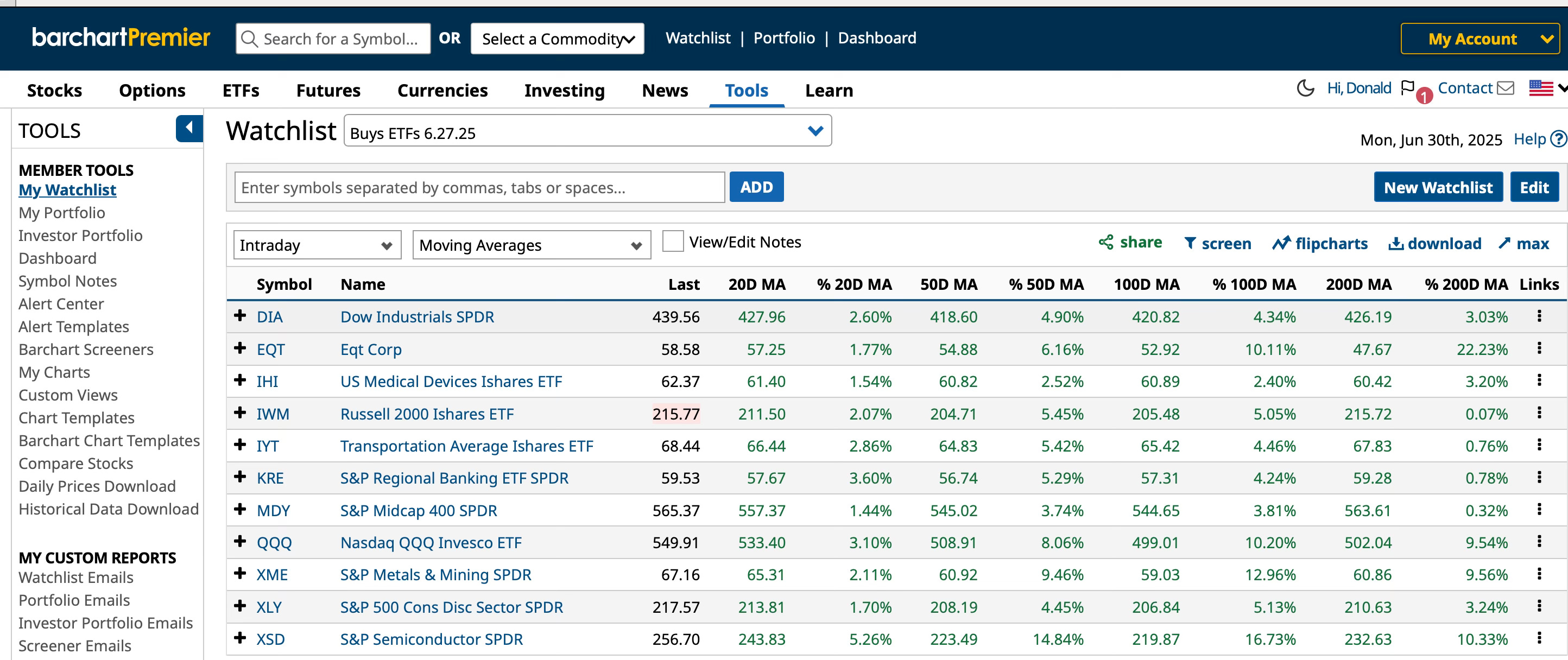

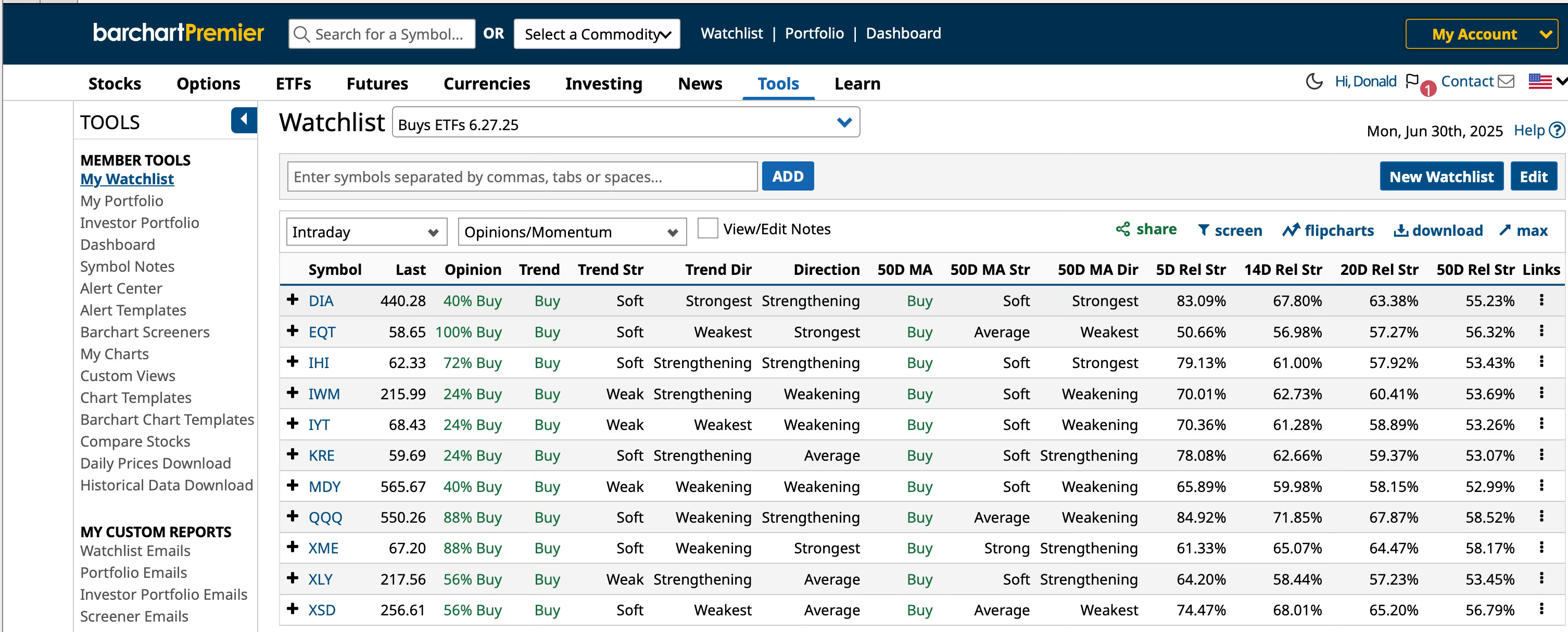

The 11 ETFs shown above all have bullish 20-, 50-, 100- and 200-day moving averages. All of the shorter duration DMA averages are higher than the next longer duration average. Zoom in on the images for better views.

Barchart.com also shows that all of the ETFs shown above are from 40% to 100% buys. That is, ETFs with 100% buy ratings have bullish ratings in each of the 13 momentum charts and other technicals that Barchart uses to track equities’ momentum. I last wrote about trading covered calls with momentum here. I wrote about selling AMZN cash secured puts here.

Investors are diversified when they trade ETFs because ETFs own dozens to hundreds of stocks.

Traders with relatively small cash reserves available to trade covered calls might buy several lower priced ETFs like EQT, IHI, IYT, KRE and XME.

Each option contract is for 100 shares. One EQT contract is for 100 shares of EQT, or $56.66 times 100 equals $5,666 per contract. For about $25,000, less the premium income, an investor can sell one contract of five of these ETFs’ puts or calls. A trader who sells one covered call ETF option and one cash secured put on the same ETF would invest about $50,000 in five trades. It is always better to do trades on several equities than on one trade. Diversification of your risks is important.

Traders seeking higher returns on risks can trade weekly options. Those who feel comfortable with longer duration options can trade monthlies. The risk in trading calls is that a bullish stock might close a lot higher than the call strike. Say you sell $100 strike calls and the ETF closes at $120. You’ve missed the upside move.

Then you either buy the calls back before expiration at a fairly high loss on the calls or let the stock be called and buy back the option at a higher price. You also can “roll” a covered call by buying a call back at a loss and sell covered calls on the next expiration dat at a higher options price.

The risk when you are selling puts is that ETF expires at a lower price than your strike price and you begin your ownership of the stock at a loss. Say you sell puts on a stock or ETF at $100 and it is at $80 when your puts option contract expires. You either take the $20 loss on the puts trade or buy the ETF at $80 and sell covered calls on it. Being down 20%, or $2,000 per puts contract is not fun, but it is manageable, especially if the ETF is in a long-term bullish trend. Another risk is that the price of the stocks soars and you would have been better off if you had bought the stock instead of selling the puts.

At the moment, EQT is trading for $58.54 per share, or $5,854 per options contract.

Since this is a holiday week, weekly traders might buy 100 shares of EQT for $58.54 a share and sell one call option on EQT with a 7.11.25 expiration date and $62 strike for about $0.26 share or $26 per contract. That would yield a 0.44% return on risk (RoR), or 19.9% annualized if the same trade was done 33 times in the next 365 days. Because prices change all day, doing the exact same trade 33 times a year is impossible, but it is something investors track.

The delta on the above trade would be about 0.16. That means there is about a 16% probability that the ETF will close above the $62 strike price and be called. If a trader wants to have the ETF called, the $59 strike calls could be sold for about $1.12 a share, or $112 per contract.

Traders who think they might be able to buy EQT at a discount could sell the EQT 7.11.25 $55 strike cash secured (CSP) puts for about $0.23 a share or $23. The delta would be about -.13, or 13%. The RoR on the 11-day trade would be about 0.42% and the ARoR would be about 19.9%, give or take. Note that the puts and calls have about the same deltas and RoR.

Traders who have more cash to put to work could do these trades on the higher priced ETFs shown above.

I’ve put more than three hours into researching and writing this newsletter.